In 2025, a donor could make a gift, report taxes the usual way, and – if they were eligible – generally get a charitable tax deduction for that gift. In 2026, that experience changes for a specific group of taxpayers. The 2026 charitable deduction still exists, but for some donors it will feel like it starts only after a small “out-of-pocket” amount – almost like an insurance deductible.

That shift is not about politics or accounting trivia. It’s about how donors think, when they choose to give, and the question many will ask this year: “So… is my gift still deductible?”

In the U.S., taxpayers generally have a choice in how they claim deductions.

Many people take the standard deduction – a fixed, preset amount that reduces taxable income automatically. It is simple and requires no listing of individual write-offs. You can give nothing to charity and still take the standard deduction.

Others choose to itemize. Itemizing means you don’t use the preset standard amount. Instead, you list specific deductible items – such as charitable gifts, mortgage interest, and certain state and local taxes – and claim the total of that list. People usually itemize only when the total of those items is higher than the standard deduction.

This distinction matters because the 2026 change we’re discussing applies to donors who itemize – not to everyone.

Starting with tax years that begin after December 31, 2025 (in other words, starting in 2026), the charitable deduction for itemizers comes with a new threshold.

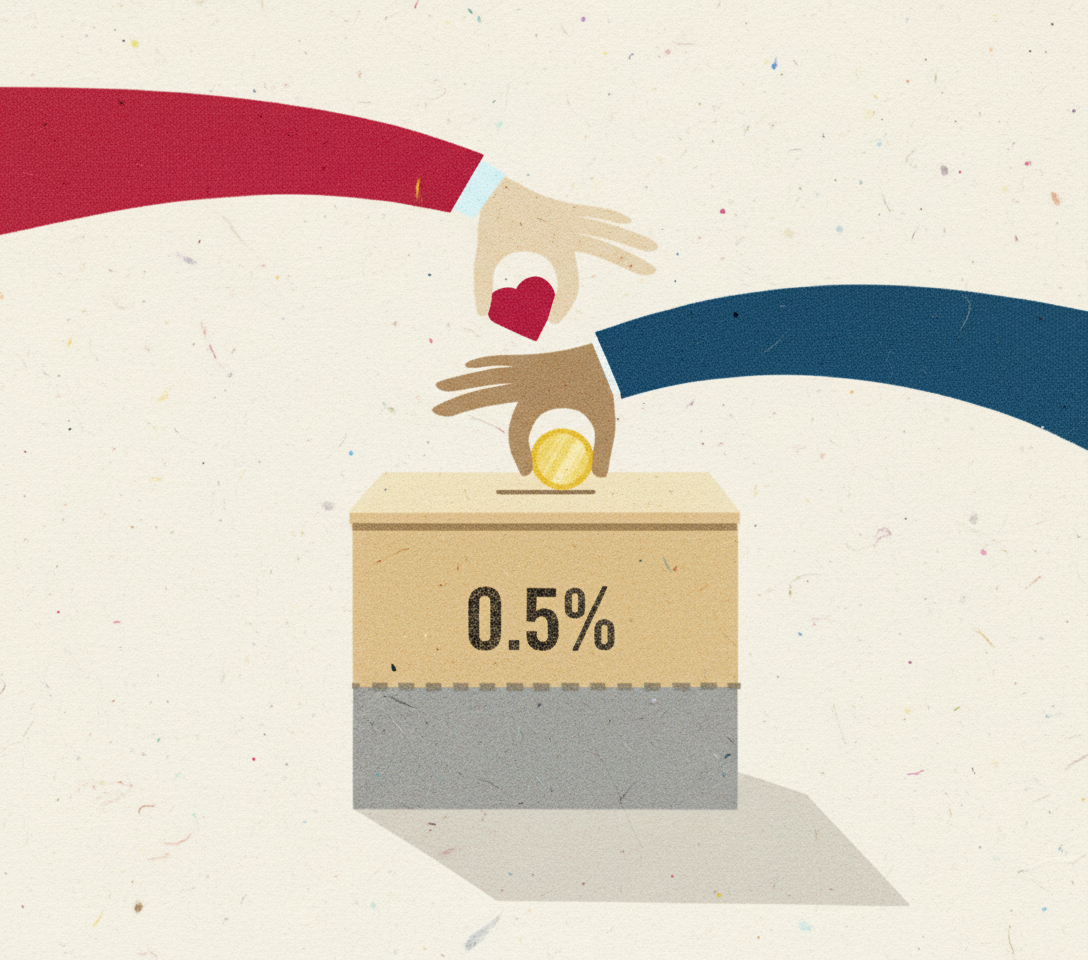

If you itemize, you can deduct charitable contributions only after your total giving for the year rises above 0.5% of a specific income baseline used in the charitable-giving rules.

Tax law calls that baseline your contribution base. For practical purposes, it closely tracks a number many taxpayers already recognize: AGI, or Adjusted Gross Income. AGI is a core IRS measure of income that shows up on the federal tax return and is used to calculate many limits and phase-ins across the tax system.

So if you don’t want to memorize jargon, the mental model is straightforward: the new threshold is roughly “half a percent of your income base.”

That 0.5% threshold is what tax professionals call a floor. A “floor” simply means a minimum level you must cross before a deduction starts to apply.

Let’s use the same kind of arithmetic donors actually use when they try to understand a rule.

Imagine a donor whose income baseline for this calculation is $200,000. Half of one percent of $200,000 is $1,000.

Under the 2026 charitable deduction rule, the first $1,000 of charitable giving does not produce a charitable deduction for an itemizer. Only the portion above $1,000 counts toward the charitable deduction.

Now take a higher-income donor with a $1,000,000 baseline. Half of one percent is $5,000. In that case, the first $5,000 of giving sits below the floor; only giving above that amount is eligible for the charitable deduction (again, under the new rule).

This is why the insurance metaphor works. Donors don’t experience the change as “my deduction shrank by 0.5% of income.” They experience it as: “The first part of my giving doesn’t count.”

Most taxpayers use the standard deduction. Itemizing is less common. In 2022, the Tax Policy Center estimated that only about 10% of taxpayers itemized.

So the 0.5% floor is not a universal donor experience. But it matters for donors who do itemize – often households with higher incomes, households paying mortgage interest, or donors who make larger gifts. For this group, the 2026 charitable deduction changes the incentives and the conversation.

The U.S. tax code has long included percentage limits on charitable deductions. In other words, the system has always had guardrails that cap how much you can deduct relative to your income base.

The new 0.5% floor doesn’t replace those rules. It simply adds a new threshold at the front end, and then the existing limitation structure continues to apply.

The net result is easy to summarize: 2026 adds a “start line” for the charitable deduction, but it doesn’t remove the other guardrails donors may already bump into.

When a system introduces a threshold, people respond in predictable ways.

First, they bunch. Instead of many smaller gifts, they consolidate into fewer, larger gifts – because crossing the threshold is what makes the benefit “turn on.”

Second, they look for vehicles that let them separate “when the tax event happens” from “when the nonprofit receives support.” In practice, that often points donors toward donor-advised funds, or DAFs.

A donor-advised fund is a charitable giving account. A donor contributes to the DAF, and then can recommend grants from that account to nonprofits over time. The structure makes it easier to time the charitable deduction while keeping flexibility about which organizations are supported and when.

This does not mean donors stop giving. It means their internal logic changes from “I give what I give” to “If I’m giving anyway, how do I make it count?”

For nonprofits, that becomes an operations and messaging challenge.

The 2026 story is not only about the new floor for itemizers. It also brings back a limited charitable deduction for people who use the standard deduction.

In practical terms, this is a small “yes, you still may get some benefit” headline for everyday donors. The amounts are capped, and it will not move major-gift strategy. But it does create a simple, donor-friendly message that many nonprofits can use without turning into tax advisors.

A safe, accurate way to say it is:

“Even if you take the standard deduction, there may now be a limited federal deduction for charitable gifts.”

Then stop. The nonprofit’s role is to point donors to reliable information and encourage them to confirm with a tax professional – not to give individualized tax advice.

Individuals aren’t the only group affected. Starting in 2026, corporate charitable deductions also have a new floor: a company’s charitable deduction is allowed only after its annual giving exceeds 1% of taxable income.

That won’t rewrite major corporate philanthropy overnight. But it can influence how some companies time smaller gifts, sponsorship-style support, or year-end contributions when finance teams optimize around tax outcomes.

Here is how to translate “a new floor” into clearer donor experience and fewer lost gifts.

Create a short “Tax note (2026)” section and keep it factual:

Confirm that the recipient organization is a recognized 501(c)(3) public charity (or, in a fiscal sponsorship arrangement, that the fiscal sponsor is the 501(c)(3) receiving the gift).

Note that tax rules changed starting in 2026, and donors who itemize may be subject to a floor before the charitable deduction applies.

Include a simple disclaimer: “This is general information, not tax advice.”

The goal is not to sell the gift. It’s to prevent donors from feeling surprised later.

Donors think in examples, not definitions. One example is often enough:

“If a donor itemizes and has $200,000 of AGI, the first $1,000 of charitable giving may not be deductible under the new 0.5% floor; amounts above that may be deductible, subject to other rules.”

You don’t need to instruct donors to bunch gifts. You can simply acknowledge that some donors choose to concentrate giving in one year and support multiple nonprofits from that pool over time.

This is where clear DAF instructions matter.

If donors are trying to “make it count,” they will use more structured paths. That makes your website and back-office process the bottleneck.

At minimum, make sure donors can quickly find:

a clean “Give via DAF” pathway,

clear instructions for gifts of appreciated stock,

a fast confirmation workflow.

For fiscally sponsored projects, clarity builds trust:

The fiscal sponsor is the 501(c)(3) that receives the donation and issues the official acknowledgment.

The sponsor maintains discretion and control, which is a standard legal requirement in fiscal sponsorship.

Donors should consult their advisors for their specific situation.

In a year when donors feel a new threshold, that kind of clean infrastructure becomes part of the value proposition.

The 2026 charitable deduction increasingly feels like it starts after a deductible because, for itemizers, it effectively does: the first 0.5% of the income baseline used in the charitable rules sits below the floor, and only giving above that line counts toward the charitable deduction.

Your job is not to turn donors into tax technicians. Your job is to keep donors from getting surpised – and to make giving frictionless once a donor has decided to support the work.